The Blue Swan Daily, in partnership with MIDAS Aviation, across this week will deliver the findings into an analysis of the world's 'Top 100' airports by capacity, highlighting differences in airport approaches to route development, passenger profile trends between different destinations, those airports that have the most reliance upon a single airline partner and those that have the biggest diversity of airline partners.

Today, we focus on Europe, the Middle East and Africa (EMEA) and look at which of the world's 'Top 100' airports have the largest and smallest percentage shares from their dominant airline partner and also look more closely at the difference between the largest European gateways.

Our analysis of OAG schedule data for the current summer 2017 schedule at the world's 'Top 100' airports by departure shows that buoyed by double-digit growth last year and in the first nine months of 2017 and the arrival of nine new airlines in the past two years, Manchester Airport in the United Kingdom has the smallest dominant airline share with its largest operator Ryanair holding just a 14.7% share of departure capacity.

Ryanair is one of 59 airlines to offer scheduled passenger flights from the main gateway to northern England with new arrivals over the past two years including Cobalt Air, Correndon Dutch Airlines, Iraqi Airways, Shaheen Air International in 2016 and Air Arabia Maroc, Freebird Airlines, the newly independent Loganair, OmanAir and the return of Royal Air Maroc in 2017.

With its strong leisure flows, Palma de Mallorca Airport (Niki - 15.5%) in Spain's Balearic Islands is second in the ranking and Moscow Domodedovo Airport (S7 Airlines - 25.4%) is ranked third.

The 'Top 10' list surprisingly also includes some of Europe's hub airports, namely Adolfo Suárez Madrid-Barajas Airport (Iberia - 27.5%) and Lisbon Airport (TAP Portugal - 32.8%), plus the Scandinavian gateways of Copenhagen Airport Kastrup (SAS Scandinavian Airlines - 27.9%) and Stockholm Arlanda Airport ( SAS Scandinavian Airlines - 34.1%).

This can be partly explained by the maturing of the Low Cost Carrier (LCC) model in Europe and the increasing competition leading airlines are finding themselves under at major airports across the Continent.

As highlighted at the start of the week, at the other end of the scale, it is Moscow Sheremetyevo that holds the crown as the world's airport with the largest dominant airline share, in its case Aeroflot Russian Airlines with a whopping 89.4% of departure seats this summer.

The big Gulf hubs of Abu Dhabi (Etihad Airways - 79.0%), Doha (Qatar Airways - 88.0%) and Dubai (Emirates Airline - 63.1%) are all among the list, as are the two largest airports in Saudi Arabia: Riyadh King Khalid International Airport (Saudia - 56.9%) and Jeddah King Abdulaziz International Airport (Saudia - 52.2%)

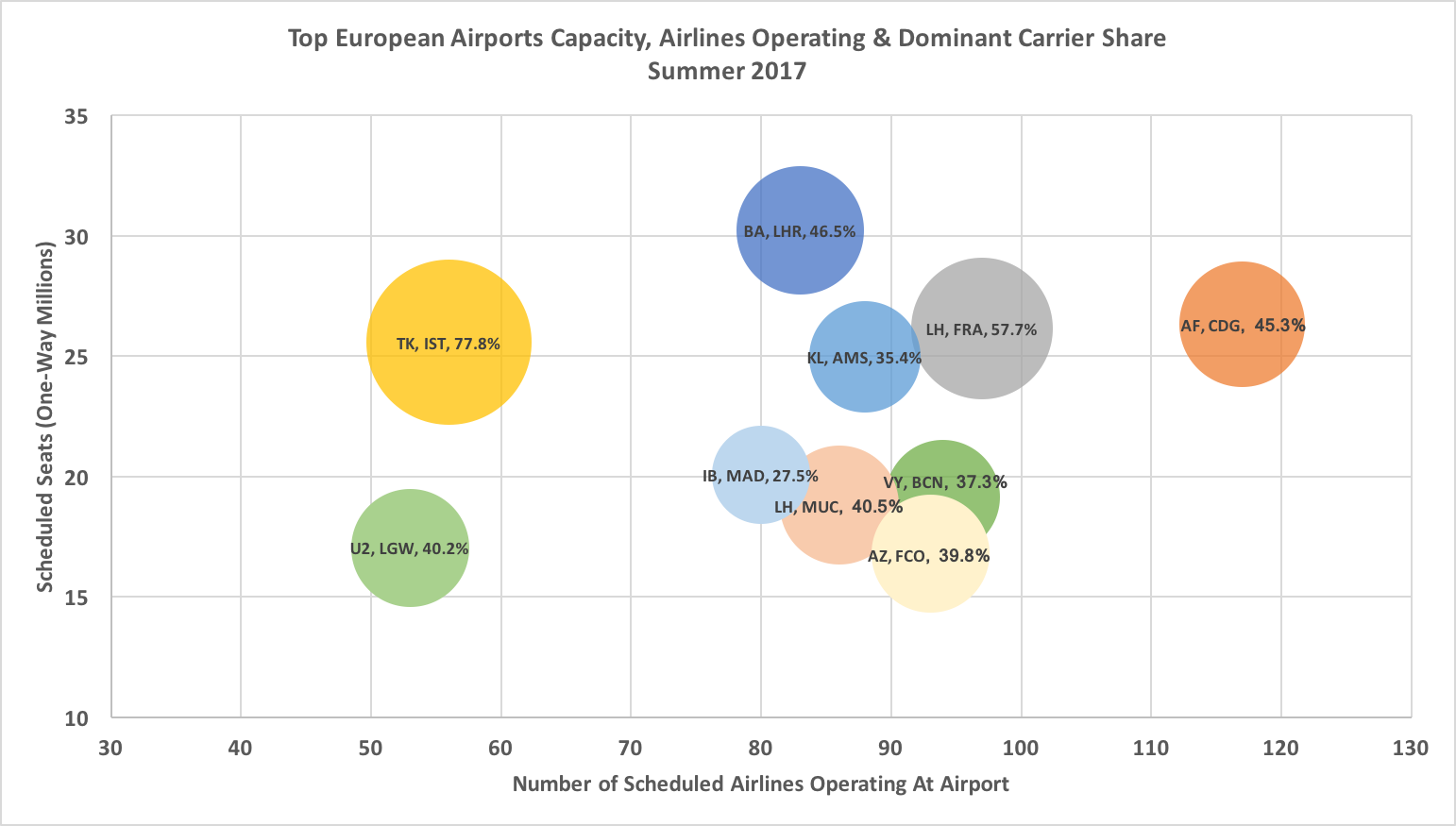

Istanbul Ataturk (Turkish Airlines - 77.8%) and Frankfurt Airport (Lufthansa - 57.7%) are also expected entries, with the German flag carrier leading the way among the traditional European flag carriers in dominating operations at one of its home hubs.

Among perhaps the 'surprise' entries in the 'Top 10' are Istanbul Sabiha Gokcen Airport (Pegasus Airlines - 64.5%), due to the split of operations by Turkey's two largest airlines between the city's two airports, and London's Stansted Airport (Ryanair - 75.3%). Interestingly, the latter's inclusion means the Manchester Airports Group's (M.A.G.) two largest airports are in the two lists, offering very different network philosophies, albeit with Ryanair as the dominant airline at both.

Other 'Top 100' major airports within the EMEA region like Brussels National (Brussels Airlines - 35.3%), Amsterdam Schiphol (KLM - 35.4%), Oslo Gardermoen (SAS - 35.7%), Zurich Airport (Swiss - 37.0%), Barcelona El Prat (Vueling - 37.3%), Dublin (Ryanair - 38.5%), Rome Fiumicino (Alitalia - 39.8%), Munich International (40.5%), Berlin Tegel (43.1%), Paris Charles De Gaulle (45.3%), Vienna International (46.3%) and London heathrow (46.5%) sit nicely between the two tables with the average dominant airline share across EMEA being 45.2% and across Europe 41.0%.

There are no African airports in the analysis as the continent's largest facilities by departure capacity in summer 2017, Johannesburg OR Tambo International Airport in South Africa (8.6 million seats) and Cairo International Airport in Egypt (7.6 million seats) were below the 8.7 million departure seat threshold to be among the 'Top 100' global airports.

CHART - Paris Charles De Gaulle Airport appears to be in the strongest position among Europe's leading hub airports with a broad variety of airline partners, but with Air France still delivering a hub model Source: The Blue Swan Daily, MIDAS Aviation and OAG

Source: The Blue Swan Daily, MIDAS Aviation and OAG

When the number of scheduled seats, the number of scheduled airlines and the percentage share of the dominant carrier are plotted on a graph in clearly illustrates some key trends and differences between the ten largest airports across Europe.

Unlike the scattered positioning of the North American hub airports in yesterday's analysis (see 'INSIGHT: The US majors and their hub domination') the ten largest European airports by departure capacity in summer 2017 are fairly centralised in the chart.

The clear exceptions are Paris Charles De Gaulle, which appears to have a solid position with a broad variety of airline partners, but with Air France still delivering a hub model; and Istanbul Ataturk Airport where Turkish Airlines dominates. In fact, the two airports are a similar scale based on the summer 2017 schedules, but the Paris gateway is served by twice as many airlines as the Turkish airport.

** TOMORROW: In Part 5 we look more closely at the biggest hub airports across the world **