Summary:

- Belgrade's Nikola Tesla Airport in Serbia is undergoing a lengthy procedure to attract bidders to a 25-year concession to manage the facility.

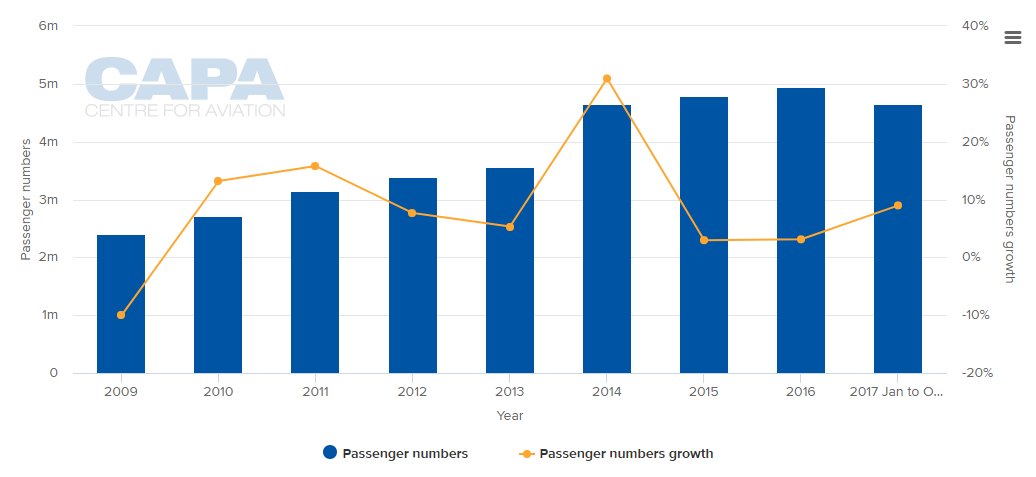

- Belgrade's Nikola Tesla Airport has seen year-on-year traffic growth every year of the current decade, including a significant surge in 2014 when passenger numbers grew 30.9%.

- The list of concessionaire bidders for Belgrade's Nikola Tesla Airport is long and impressive, but does history in the region cast clouds over the whole process.

One of the main reasons cited is unfamiliarity with local financial and legal customs and practices, a feeling of being "out of our comfort zone". The same couldn't happen with investors into European airports. Or could it? Indeed, should it?

Presently, Belgrade's Nikola Tesla Airport in Serbia is undergoing a lengthy procedure to attract bidders to a 25-year concession to manage the facility. It is not the only airport in East Europe to be doing so; others include the main airports in Lithuania, where the procedure is crawling along at a snail's pace, while the 35-year concession on Sofia Airport was cancelled owing to "unforeseen circumstances" in Apr-2017.

On the face of it the Belgrade concession should be an opportunity for investors. As long ago as Mar-2015 a CAPA - Centre for Aviation report entitled 'Belgrade Airport, with resurgent Air Serbia, challenges the hub order in Central/Southeast Europe', found that the Nikola Tesla Airport was "challenging the hub system in Central and Southeast Europe".

What had prompted that report was a sudden surge in passengers in 2014, over 30%. But, as the chart below shows, traffic stabilised in the aftermath, though it has increased again in the first ten months of 2017, by 9%.

CHART - Annual passenger traffic growth at Belgrade's Nikola Tesla Airport peaked in 2014 as national carrier JAT Airways was remodelled as Air Serbia under the influence of Etihad Airways Source: CAPA - Centre for Aviation and Belgrade Nikola Tesla Airport

Source: CAPA - Centre for Aviation and Belgrade Nikola Tesla Airport

What's more though, the airport is profitable; its net profit increased by 12% in the first 10 months of 2017, in line with the passengers numbers increase, to EUR25.1 million.

The list of concessionaire bidders is long and impressive. They are known to include:

- Consortia made up of:

- Zurich Airport, Meridian Infrastructure Fund and Eiffage;

- GMR Infrastructure and GEK Terna;

- Incheon International Airport Corporation, Ic Ictas Altypi and VTB Capital;

- HNA Airport Group, AVIC International Holding Corporation and Chinese-ASEAN Investment Corporation Fund;

- A stand alone bid by VINCI Airports.

Notable amongst them are Zurich Airport, which has been active in airport privatisation for two decades, Russia's VTB Capital in one of its first ventures outside Russia, the collective interest from China, and Vinci Airports, one of the world's leading airport investors right now.

And yet, the date for the submission of binding tenders has been put back three times, from early September to 08-Dec-2017, the Minister of Construction, Transport and Infrastructure saying that he "supports giving investors extra time to get the best deals."

The big question is for whom - the investors or the airport? One sticking point may be the expectation that the winning bidder will "extend the boundaries of development, which we have laid the foundations for." That seems to be a reference to the refurbishment of terminals 1 and 2, at a combined cost, including associated works, of over USD50 million. How far are they expected to be extended is unclear?

While the capability now exists to handle long-haul traffic, Air Serbia, which has over half the capacity at the airport won't be doing that to any great degree. The carrier has only one wide body jet in service and none on order (though it could deploy A320neos on some medium and long sector routes) serving its Belgrade-New York route.

Recently the airline has been refocusing on short haul routes and on increasing code shares. LCC penetration is low in Serbia generally, another bridge for a concessionaire to cross.

The interest from China is critical. Air Serbia considered a direct service to China in 2016 but the proposition was dismissed by the Prime Minister early in 2017 and instead a Hainan Airlines (part of HNA Group) service between Beijing and Belgrade was discussed at the World Economic Forum in Davos. That would seem to put the Chinese consortium in pole position amongst the bidders and the Chinese are attracted generally to central European locations for airfreight purposes (they are also looking at Serbia's Uzice Ponikve Airport, which does not handle commercial traffic).

MAP - The urban area of the City of Belgrade has a population of 1.23 million, while over 1.68 million people live within its administrative limits Source: Google Maps

Source: Google Maps

But another factor must be whether or not Serbia will be allowed to join the European Union. Formal negotiations commenced in 2014, with the possibility of accession by 2025. However, support within Serbia itself has diminished and there is no certainty there will even be a European Union in 2025. That would remove from the equation a pre-requisite of many, if not all, of the bidders.

Those bidders with unexpected time on their hands might want also to contemplate some of the failed deals in this part of the world, such as the invalidation of the 2006 concession on the Bratislava and Košice airports in Slovakia on the grounds that the sale had not been approved by the country's antitrust authority. The Slovakian Prime Minister, with refreshing candour, declared the sale had been "a big mistake" and that the airports "belong to the Slovak Republic."

Or even the cancellation of the privatisation tender for Budapest Airport the previous year and the lingering threat of renationalisation that hung over the transaction for years after it was finally completed.

Airport financing is at the whim of governments the same as everything else; there are unstable ones in this region as there always have been and they can change suddenly and diametrically. It is incumbent on all bidders to do their due diligence thoroughly and not only on the profit and loss account and balance sheet.