Long-haul markets remain strong and are helping to drive the passenger numbers up with traffic to the Middle East and East Asia growing by almost 10% and more than 5% respectively. Airlines on these routes are making the most of their slots by switching to larger aircraft, while a number of slots previously used for short-haul operations in Europe have been sold to long-haul operators using widebodied equipment.

Despite the record performance its existing capacity constraints have significantly blunted growth at Heathrow and has seen Dubai International overtake it as the world's largest international airport and Amsterdam Schiphol take on the position as Europe's best connected hub airport. Despite the restrictions Heathrow is still growing even before a long-awaited potential third runway is built.

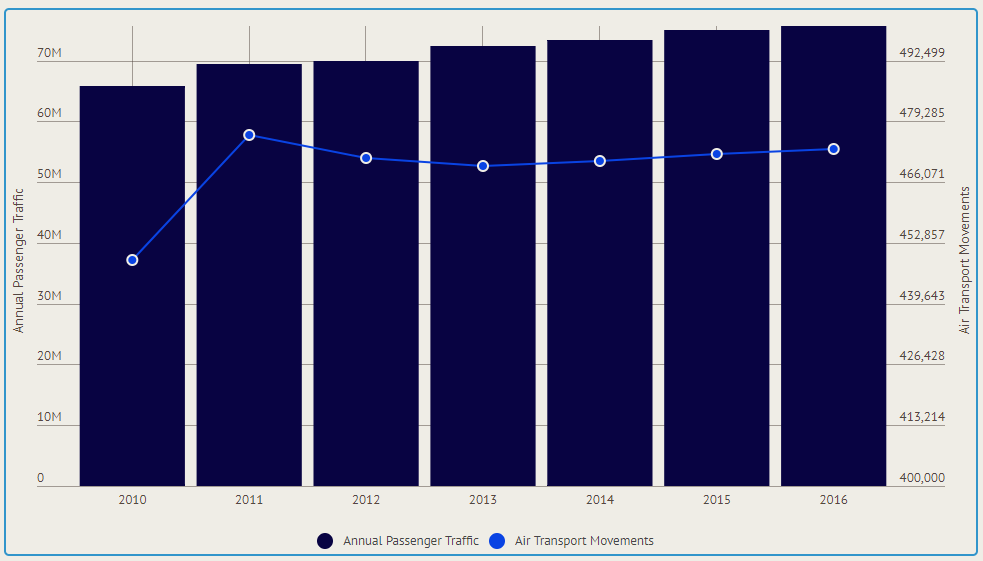

CHART - London Heathrow Annual Passenger Traffic and Air Transport Movements (2010 - 2016) Source: The Blue Swan Daily and Official Airport Data

Source: The Blue Swan Daily and Official Airport Data

Over the last ten years passenger traffic at London Heathrow has grown 12.4% from 67 million annual passengers in 2006 to over 75.5 million last year. It has witnessed year-on-year growth in every year of the current decade, albeit at an average annual rate of 2.4%. As a comparison, over this decade Dubai International has grown 77.0% from 47 million annual passengers in 2010 to over 83 million last year, growing at an average annual rate of 10.0% this decade. Over the first four months of 2017 traffic is up 7.8%.

Heathrow's unique capacity constraints - it is operating at 98% capacity - coupled with the high demand from airlines due to strong passenger yields at the airport, mean slots are hard to obtain. The airport currently claims it has a queue of 30 airlines waiting for slots and in the past couple of years Oman Air paid a reported $75 million for morning inbound and outbound slots to launch a second daily rotation in and out of the hub from and to its Muscat base. Croatia Airlines and SAS Scandinavian Airlines are among carriers that have sold slots for financial gain.

It's estimated that due to demand from airlines and passengers to use the airport far outstripping supply, passengers are already paying on average £95 more per a return ticket then if Heathrow had extra capacity (Frontier Economics, 2014: Impact of airport expansion options on competition and choice).

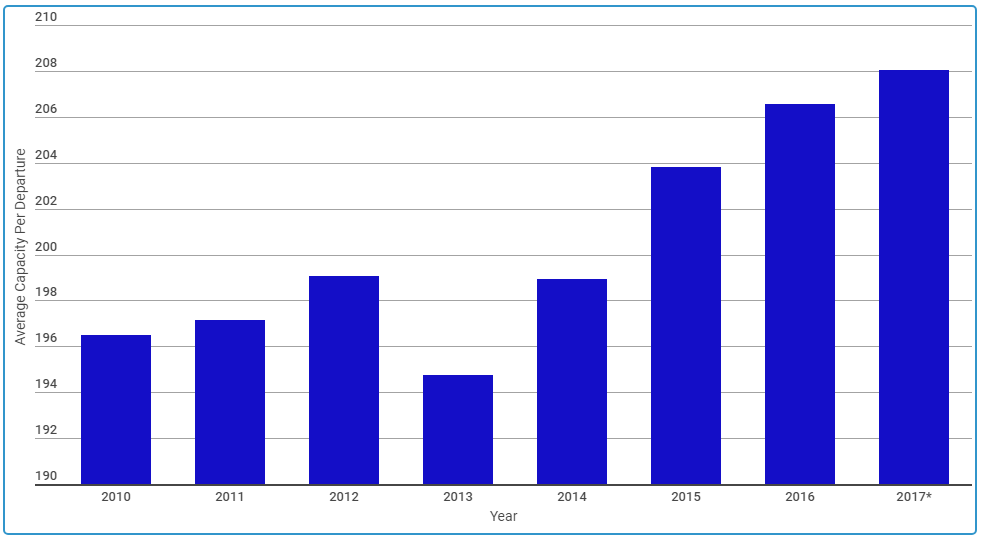

Maximising the use of each slot has seen the average size of aircraft operating from Heathrow rise from 190.4 seats per departure in 2006 to 206.6 seats in 2016, according to The Blue Swan Daily analysis of data from OAG.

CHART - Average Aircraft Size per London Heathrow Departure (2010 - 2017) Source: The Blue Swan Daily and OAG Schedules Analyser

Source: The Blue Swan Daily and OAG Schedules Analyser

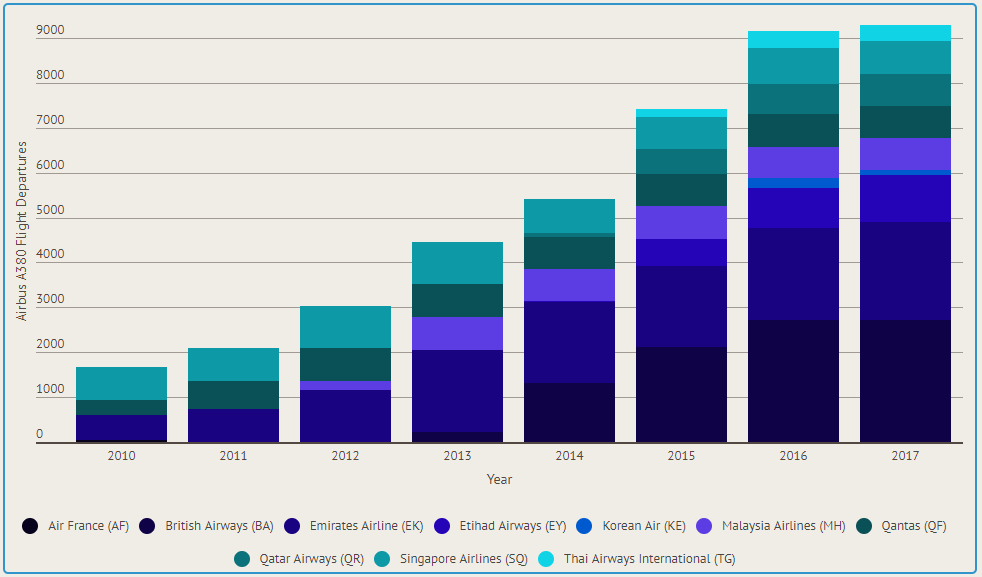

This growth has been supported by the growing number of Airbus A380 flights now scheduled (up to 9,151 departures in 2016; 25 a day), making the facility the second largest market for Superjumbo operations. The average aircraft size is forecasted to rise further to 208.0 seats per departure for 2017, based on published schedules, despite multiple-daily turboprop operations now offered by Flybe on two domestic routes to Scotland.

CHART - Annual Airbus A380 Flight Departures from London Heathrow (2007 - 2017) Source: The Blue Swan Daily and OAG Schedules Analyser

Source: The Blue Swan Daily and OAG Schedules Analyser

Despite the strong demand, OAG data shows the number of departures from Heathrow has actually declined over the past couple of years after reaching a high of 239,002 annual departures in 2011. This record year for movements pipped the 2007 performance by just two outbound flights. Annual growth in movements returned in 2015 with a 0.4% year-on-year growth, followed by another 0.4% uplift last year. This year's published schedule forecasts a 0.6% rise.

This may appear seem surprising. However, as the airport is operating at such a high capacity slot availability remains limited to times of the day not suitable to many operators for sustainable schedules and the airport is effectively full during peak demand periods. The recent growth has been facilitated by additional off-peak slot usage and the return to operation of the remedy slots made available following the acquisition of bmi british midland by BA parent IAG.

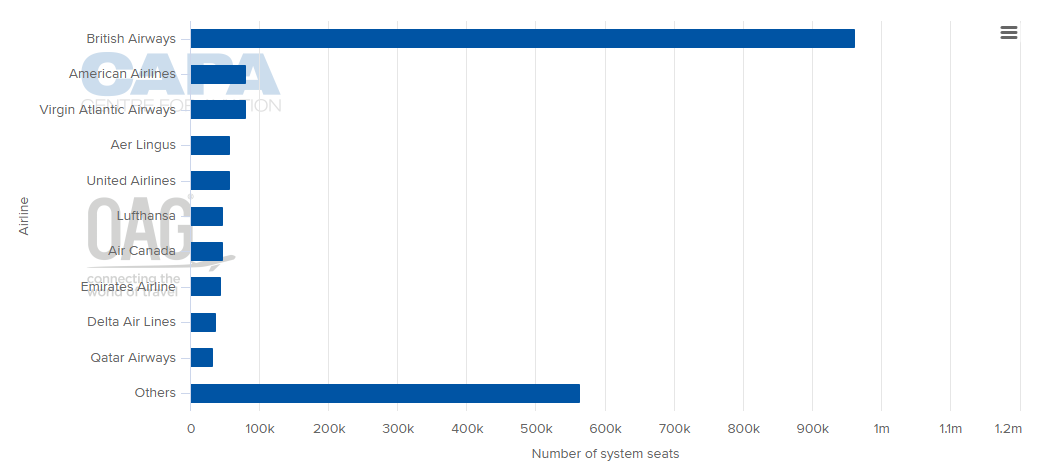

CHART - Largest Operators from London Heathrow (weekly seats) Source: CAPA - Centre for Aviation and OAG

Source: CAPA - Centre for Aviation and OAG

Latest schedules show British Airways (BA), the largest operator at Heathrow with a 47.8% capacity share, has grown its inventory at the hub airport by 24.2% since the start of the decade, a period that has actually seen ten new airline brands start flying from the airport. Over the first four years of the 2010s fellow UK carrier Virgin Atlantic Airways had grown 42.4%, although a network restructuring has meant capacity has subsequently declined by around a third and will this year retreat to levels last seen back in the 2000s.

The largest capacity growth among the top twenty carriers at the airport since 2010 has unsurprisingly come from the world's new hub carriers: Qatar Airways (+94.5%), Etihad Airways (+85.0%), Turkish Airlines (+74.4%) and Emirates Airline (+53.9%). The US majors have also significantly grown their presence - Delta Air Lines (+66.7%), United Airlines (+33.5%) and American Airlines (+32.5%), while elsewhere KLM (+31.2%) has grown by almost a third, mainly through upgauging.

Outside the top twenty carriers at London Heathrow, significant growth has been recorded since 2010 by China Eastern (+155.1%), Azerbaijan Airlines (+145.3%), Air China (123.7%), Air Astana (115.0%), Aegean Airlines (+83.1%), Ethiopian Airlines (+78.1%), Aeroflot Russian Airlines (+77.1%). New arrivals have included the Eurowings and Germanwings brands as part of Lufthansa's restructuring of its non-hub flying, plus Aeromexico, Avianca, China Southern Airlines, Flybe, Garuda Indonesia Airlines, LAN Airlines, Philippine Airlines and Vietnam Airlines.

While we regularly look at the value of international connectivity and its important role in international trade, this year's schedules include the arrival of UK regional carrier Flybe, which with operations across nine months of the year is already among the top 50 operators at London Heathrow with more seats than the likes of Korean Air, Air New Zealand and SriLankan Airlines.

The airline is using the remedy slots from the IAG acquisition of bmi british midland that had previously been used unsuccessfully by Virgin Atlantic Airways under its Little Red domestic brand. They are being utilised to provide up to 25 return flights per week between Edinburgh and London Heathrow and up to 20 return flights per week between Aberdeen and London Heathrow with up to four and three daily rotations on each route, respectively.

Flybe's arrival shows that recent measures such as Heathrow's £10 reduction on domestic passenger charges are working to deliver improved local connectivity. In the last month alone it has flown more than 22,000 passengers on its two routes, stimulating demand. It hopes to grow its network once a three-runway Heathrow operation becomes a reality offering enhanced regional UK connectivity via Heathrow to the rest of the world.

This will help London Heathrow to once again build its connectivity, having slipped behind Amsterdam Schiphol in terms of direct connectivity in Europe and remain below Frankfurt, Amsterdam, Paris CDG and Istanbul Ataturk in terms of its hub connectivity, according to the latest ACI Europe Connectivity Report. Amsterdam's rise from 6th position back in 2007 has been driven by significant network growth feeding its hub connectivity, but is also reflective of the fact that LCCs now account for 21% of the airport's direct connectivity - the highest LCC direct connectivity share amongst any European major airport.

The ACI Europe Connectivity Report says that over the past 10 years, 99% of the growth in passenger traffic of the top 20 European airports has been delivered by low cost carriers, something that London Heathrow has missed out upon due to its capacity constraints and resultant high fees. "Low cost carriers have moved into larger airports and hubs," says Olivier Jankovec, director general, ACI Europe. "The low cost revolution is marching on - and nothing will stop it."