The 2020s will transition to a "decade of delivery" for London's largest air gateway, according to Heathrow airport CEO John Holland-Kaye as a potential, long-awaited third runway could bring a much-needed capacity boost to the facility. That third runway, explains Mr Holland-Kaye will give Britain "more hub capacity" than rivals in France or Germany, making it "the best connected country in the world".

Alongside facilitating improved domestic connectivity, new regular, direct flights to "all the major cities in the US, India and China - the great economies of the 21st Century - will put all of Britain at the heart of global trade and we look forward to delivering this economic growth," according to Mr Holland-Kaye.

Heathrow has submitted an initial business plan to the UK Civil Aviation Authority (CAA) showing how the airport will deliver expansion and connect all of Britain to global growth. The plan illustrates lower fares for passengers with new capacity and shows how expansion is sustainable, affordable, financeable and deliverable.

However, the CAA has rejected aspects of the proposal, especially relating to a request to increase spending in fear that passengers could ultimately be forced to pay for much of the additional investment. In a consultation published by the CAA, it said "the best approach in the interest of consumers" is to limit certain early construction costs.

The consultation also said an assessment by an independent fund surveyor of Heathrow's plan to open a new runway by 2026 was an "aggressive schedule" which would require "maximum activity" even before the airport knew whether it had been granted a development consent order. Instead it now appears that should final development consent be awarded it is unlikely the new runway will be operational before early 2028, more likely in 2029.

For some even those delayed targets are ambitious. Emirates Airline's president Sir Tim Clark said "2035, if you're lucky" when questioned last year on the likely opening date of the runway, and added: "I'm not altogether sure that it will happen". IAG CEO Willie Walsh has also hit out at the cost of the project. Both will be retiring from their roles this coming summer, but their replacements will likely continue the rhetoric.

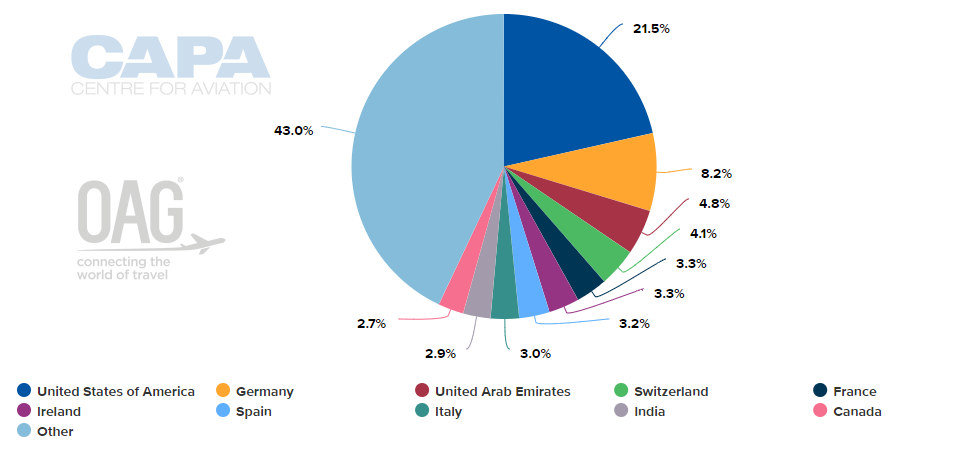

CHART - The United States of America is the largest market from London Heathrow and accounts foe one in five departure seats from the UK hub Source: CAPA - Centre for Aviation and OAG

Source: CAPA - Centre for Aviation and OAG

Heathrow is to launch an eight-week public consultation "finalising" its proposals for airport expansion between Apr-2020 and Jun-2020 and responses will be feed into a final planning application which will be submitted to the Planning Inspectorate "towards the end of 2020".

The UK Parliament gave the go-ahead last year for the expansion of the airport, but campaigners trying to block the plan, including a group of councils, environmental charities and Mayor of London Sadiq Khan, are bringing a legal challenge over the former Government's approval.

For now, Heathrow continues to squeeze out capacity gains. Over the past decade, Heathrow has welcomed an additional 15 million passengers - an increase of 18% over the period, facilitated by GBP12 billion worth of private investment which included the opening of the new Terminal 2, the Queen's Terminal, in 2014.

Last year, passenger numbers edged up +1.0%, with the strongest annual gains being seen in Africa (+5.1% year-on-year), North America (+4.1%) and Latin America (+2.3%). There were also gains in Middle East (+1.2%) and domestic (+0.9%) traffic, but falls in European Union (-0.5%) and non-European Union (-0.5%) traffic and to Asia/Pacific (-1.1%).