The largest growth markets are spread across the world with Western Europe leading the way with an additional 13.1 million LCC seats, South East Asia with 11.2 million additional LCC seats, North East Asia with 11.0 million more LCC seats and North America with 9.0 million additional available LCC seats. In terms of growth rates the largest rises in winter 2017/2018 LCC capacity versus winter 2016/2017 are being seen in Central and Western Africa, up +35.8%; North Africa, up +22.4%, North East Asia, +20.5%; Southern Africa, +19.7%; and Eastern and Central Europe, up +18.9%.

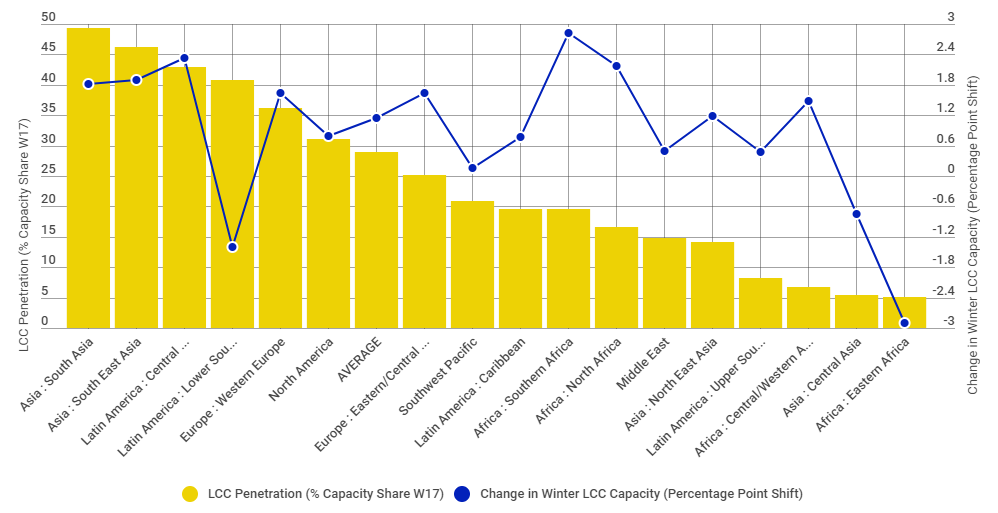

LCCs are now responsible for more than one in every four seats being flown, a figure that is sure to grow as the sector continues to mature in established markets and continues to grow in emerging economies. The LCC model's greatest penetration by capacity is across South Asia with a 49.3% share of total seats, ahead of South East Asia (46.3% share), Central America (42.9%) and Lower South America (40.9%).

CHART - Six regions of the world have a stronger than global average level of LCC operations; dominated by the Asian and Latin American markets, ahead of the more mature Western European and North American industries Source: The Blue Swan Daily and OAG

Source: The Blue Swan Daily and OAG

There are only four regions of the world where LCC penetration is in single digits and half of these are in Africa. The lowest global LCC voids are in Eastern Africa, where LCC's hold just a 5.0% share of total capacity and Central Asia with a 5.4% share. Both markets are seeing declines in LCC capacity and penetration in winter 2017/2018 versus winter 2016/2017 (Eastern Africa: -29.5% capacity decline and -2.9% fall in LCC penetration share; Central Asia: -6.4% capacity decline and -0.8% fall in LCC penetration share). The other two regions with a single digit LCC penetration comprise Central and Western Africa (6.8% share and 1.5 percentage point growth) and Upper South America (8.1% share and 0.5 percentage point growth).

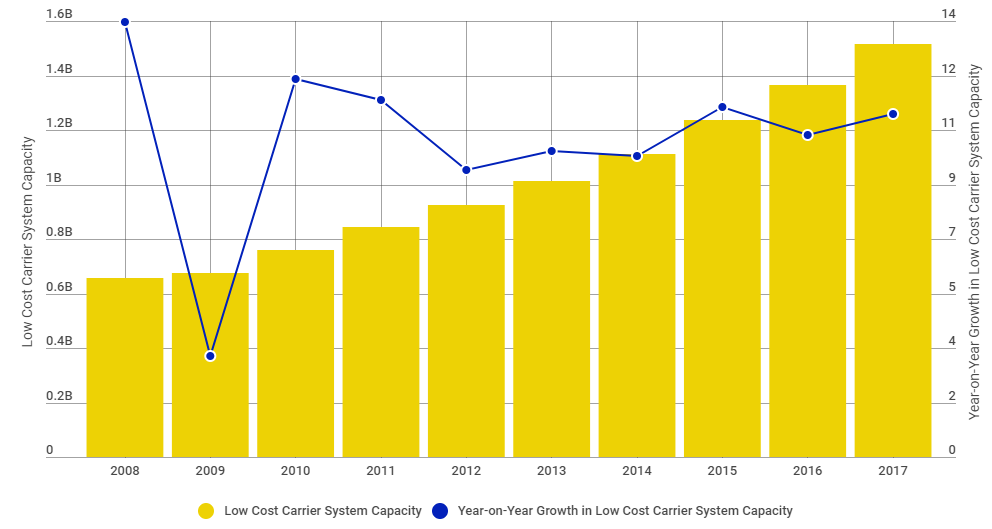

As reported by The Blue Swan Daily earlier this year, the number of LCC seats on sale in 2017 exceeded 1.5 billion for the first time ever as the global seat capacity of the world's LCCs grew 11.0%, a third successive year over double-digit growth. In fact LCC capacity has been growing at an average annual rate of 10.2% over the last ten years almost tripling in size from 575 million seats in 2007. This has seen the LCC share of the growing air transport market increase from 16.5% in 2007 to 28.7% last year and now spreads to around 160 global nations.

CHART - The number of global seats flown by low cost carriers continues to rise strongly with an average annual growth in double digits over the past ten years Source: The Blue Swan Daily and OAG

Source: The Blue Swan Daily and OAG

The United States of America (USA), India, Indonesia, Spain and the United Kingdom (UK) remain the five largest LCC markets across the globe, albeit Spain did jump above the UK into fourth position. The rest of the top ten comprises China, Brazil, Italy, Thailand and Germany.

It is no surprise to learn that China was the fastest growing of these markets in 2017 (up +25.1% versus 2016 and up from 18th position at the start of the decade to 6th position in 2017 and likely to overtake both Spain and the UK in the coming years. Together these ten country markets account for a 62.5% share of the total LCC market and were responsible for almost 95 million of the 150 million additional seats added in 2017.

Where are LCCs strongest among world's largest airports?

The Blue Swan Daily takes a closer look at the world's biggest airports to see where LCCs are dominating. Among the world's top 50 airports by capacity this winter there are five where LCCs have a greater share of departure seats than their traditional competitors.

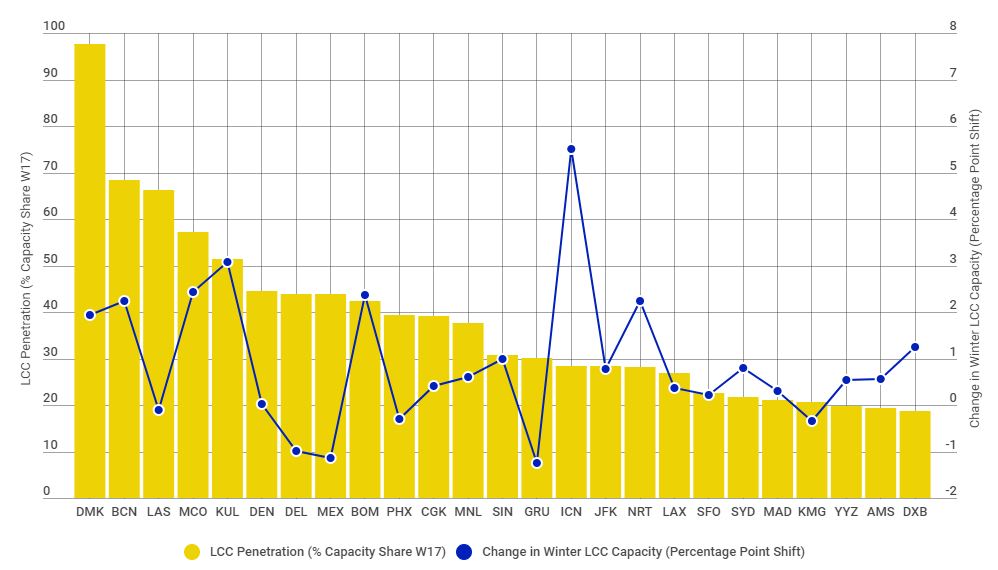

CHART - Across the world's top 50 airports by capacity, LCCs account for a 21.5% share of the total seat inventory holding a dominant share at five Source: The Blue Swan Daily and OAG

Source: The Blue Swan Daily and OAG

Topping the list is Bangkok's Don Mueang International Airport, the former primary hub for the Thai capital, but now a LCC playground. This winter LCCs account for a whopping 97.6% of the capacity, and that is up 1.9 percentage points on last summer.

Other standout major airports for LCC operations are Barcelona El Prat in Spain (with a 68.5% share), Las Vegas McCarran International Airport in USA (66.1% share), Orlando International Airport in USA (57.2%) and Kuala Lumpur International Airport, the primary gateway to Malaysia (51.4% share).

At the other end of the scale, at Beijing Capital International Airport in China LCCs account for just a 0.6% share of total capacity, while London Heathrow in the UK (2.1%), Charlotte-Douglas International (3.0%), Miami International (4.1%) and Dallas-Forth Worth International (4.3%), all in the USA, are among 18 of the top 50 airports to have a LCC share of less than 10%.

The largest growth in LCC penetration in winter 2017/2018 (versus winter 2016/2017) is being seen at Incheon International Airport, serving Seoul in South Korea, where the LCC share has grown 5.5 percentage points. In total 36 of the world's top 50 airports are seeing an increase in LCC penetration with the Frankfurt hub in Germany (3.8 percentage points) and Kuala Lumpur International (3.1 percentage points) holding the other podium positions. The largest decline in LCC share is being seen at São Paulo/Guarulhos-Governador André Franco Montoro International Airport in Brazil (down 1.2 percentage points).

What are the world's largest airports for LCC operations this winter?

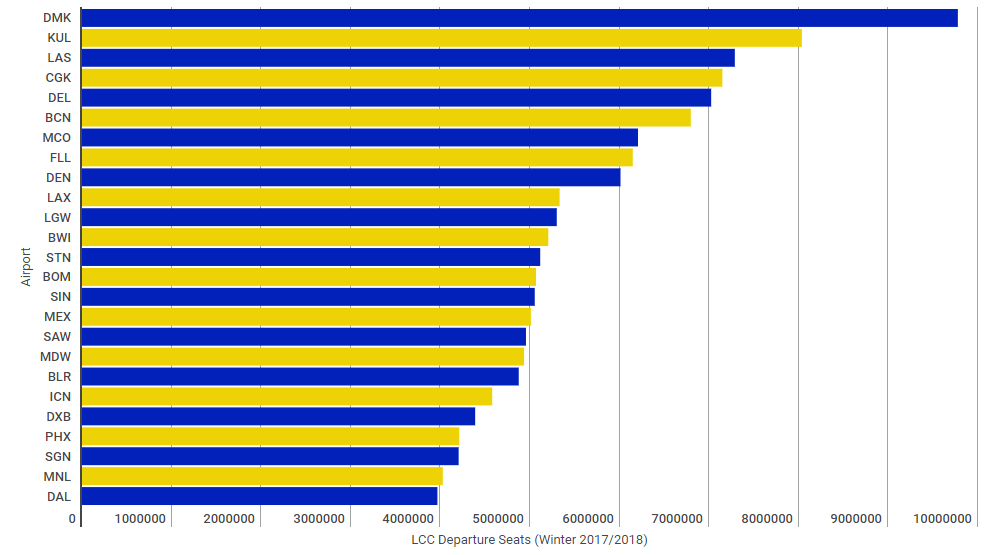

Bangkok's Don Mueang International Airport again leads the ranking with over 9.7 million departure seats on offer from LCCs this winter. Kuala Lumpur International Airport is again ranked highly with 8.0 million seats with Las Vegas McCarran International holding the last podium position with 7.2 million available seats. A total of 16 global airports are offering more than five million LCC seats this winter.

CHART - Four of the top five airports for LCC operations are located across Asia and five of the top ten are in the USA Source: The Blue Swan Daily and OAG

Source: The Blue Swan Daily and OAG

LEARN MORE about LCCs at CAPA's Global LCC Summit

At CAPA's Global LCC Summit, LCC CEOs and experts from every continent will meet to discuss the key directions the industry is taking. This is a new event for CAPA, complementing its existing suite of global strategic industry forums held in key markets across the world, highlighting the increasing importance of the LCC sector in the global aviation market.

The conference will take place at the Capella Singapore on March 1/2, 2018. You can view the full agenda, already registered speakers and register on the Global LCC Summit landing page.