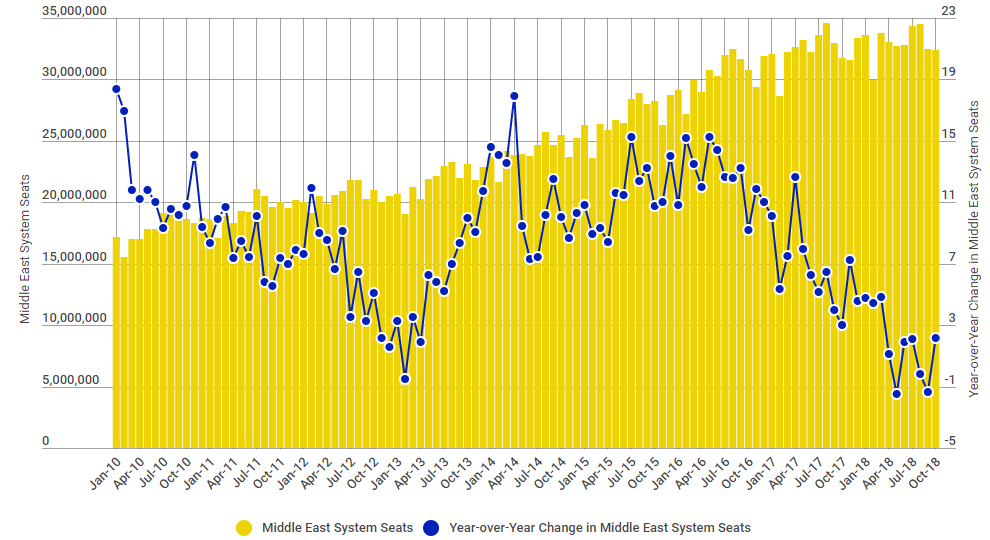

It is clear the ambitious network growth strategies among the Gulf hub carriers - based on sixth freedom rights via their respective hubs - is continuing to drive capacity growth in the Middle East. The number of non-stop seats available in the region has more than doubled over the past ten years rising from 169 million in 2008 to 388 million last year, according to flight schedule data from OAG. But, how much longer can such growth rates be sustained?

Annual growth rates in capacity have actually exceeded +6% every year since 2008 reaching double-digits in 2014, 2015 and 2016. This slowed back to a still healthy +6.6% rate in 2017, but, there are now suggestions this market may has reached a plateau? Can we expect much shallower future growth from a region that has shown strong performance and which has been at the centre of aviation growth this past decade?

An investigation by The Blue Swan Daily into current OAG flight schedules shows that Apr-2018 could be the first month since Feb-2013 to see a decline in year-over-year capacity to, from and within the Middle East. Influenced by comparing to one of only two double-digit monthly year-over-year rises last year, current published schedules show that capacity is predicted to fall -1.5% in Apr-2018 compared to last year. Although future schedules show a modest return to growth in May-2018 and Jun-2018, declines could return in Jul-2018 and Aug-2018.

CHART - Annual network capacity growth in the Middle East fell to its lowest rate in Oct-2017 and has remained shallow during the first months of 2018. Future published schedules suggest these rates will reduce further in the year ahead and could go into the red Source: The Blue Swan Daily and OAG

Source: The Blue Swan Daily and OAG

This is all hypothetical, of course, as it is always difficult to compare future schedules with historic data. But, it does support a general slowing of aviation growth across the Middle East. We last saw a considerable slowing in Middle East capacity growth over the first three months of the decade, which culminated in the year-over-year decline in Feb-2013. But, the market rebounded quickly with regular double-digit year-over-year growth rates being recorded in 2014, 2015 and 2016.

In fact the intra-Middle East market actually recorded its first recent annual year-over-year decline in capacity in 2017. This was influenced by the Qatar blockade which has ended all air connectivity between Qatar and Bahrain, Egypt, Saudi Arabia and the United Arab Emirates (UAE) and has clearly impacted the market. Having grown more than 50% since the start of the decade, with an average annual growth of +6.3%, capacity levels slipped by -8.3% in 2017.

This has accelerated a trend that was already seeing capacity linking the Middle East to the rest of the world growing faster than the market within the region. This had already seen the local capacity share of departure seats fall from a majority position at almost 55% in 2010 to a minority share of just over 48% in 2017. This fell to 45.4% in 2017, the fastest rate of annual decline this decade.

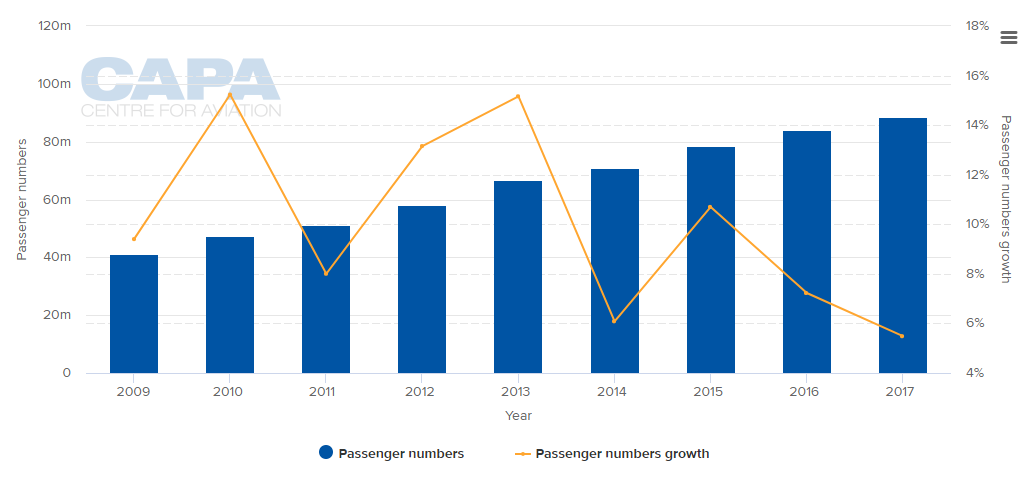

CHART - The growth in traffic at Dubai International Airport has been phenomenal, although the rate of growth slipped to its lowest level this decade in 2017 Source: CAPA - Centre for Aviation and OAG

Source: CAPA - Centre for Aviation and OAG

The rise in passenger traffic at Dubai International Airport is a good example of the rise of aviation in the Middle East. Around ten years ago it was handling 34 million passengers a year, but now handles more than 88 million. Despite a slowing of its growth (and a small decline in traffic in the first month of 2018 versus Jan-2017) , its operator Dubai Airports predicts that the growing partnership between its two largest carriers, Emirates Airline and flydubai, could help it return to double digit growth in 2019 and help it grow beyond 100 million annual passenger.

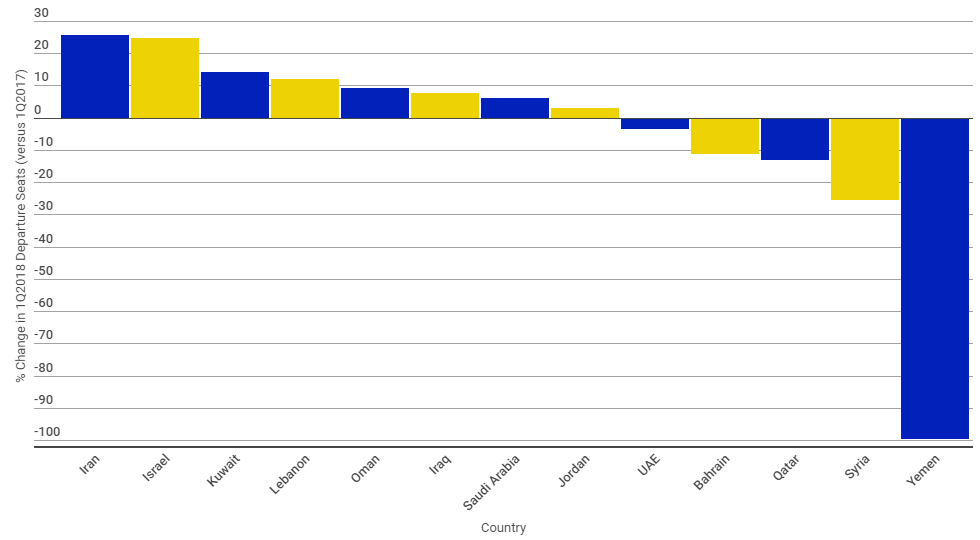

While Dubai International dominates as the busiest airport in the region with a 22.4% share of departure capacity across 1Q2108, it is Iran that has the largest count of additional available departure seats during the period as it continues to open its doors to air connectivity.

CHART - Iran and Israel have seen the largest increase in year-over-year departure capacity in 1Q2018, a period when major markets such as UAE and Qatar have seen inventory declines Source: The Blue Swan Daily and OAG

Source: The Blue Swan Daily and OAG

The Blue Swan Daily analysis shows 1Q2018 departure capacity up by a quarter (+25.8%) versus the same period in 2017, adding an additional 1.6 million seats and in the process overtaking Qatar as the third largest market in the Middle East by departure seats. Its growth rate is just ahead of the +24.6% recorded by Israel in 1Q2108; the latter buoyed by the growth of low cost airlines in the country.

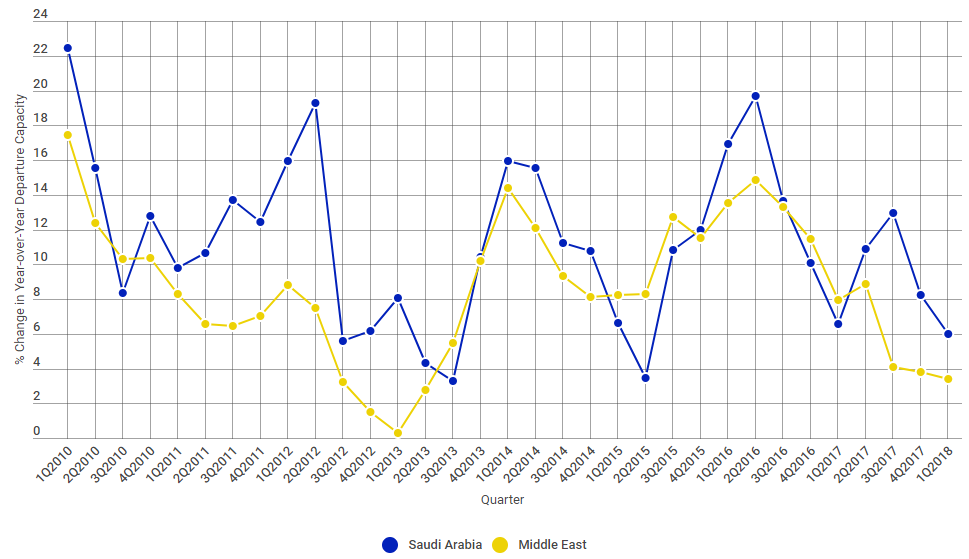

Saudi Arabia also continues it remarkable rise as tourism becomes a key pillar of its economic development. An additional 925,000 additional seats were available in 1Q2018, a growth of +6.0% versus the same period last year. This continues an amazing growth that seen 36 consecutive quarters of year-over-year capacity growth dating back to 2009 and which has influenced the regional performance. In fact in 23 of those quarters growth were at double-digit levels with an average quarterly growth of +12.0% during the period.

CHART - The Saudi Arabian aviation sector has been growing at a rapid rate this decade and strongly influenced the performance of the Middle East market Source: The Blue Swan Daily and OAG

Source: The Blue Swan Daily and OAG

WANT MORE INDUSTRY INSIGHT AND ANALYSIS ? - For more detailed insights into industry trends and detailed analysis on the industry's major talking points sign-up for a CAPA - Centre for Aviation membership.