Both Delta Air Lines and Untied are warning that challenges are arising on trans-Atlantic routes after their respective unit revenue performance in those markets during 4Q2018 fell drastically from strong results posted earlier in the year. And with growing uncertainty over the fate of Brexit, headwinds in the trans-Atlantic could intensify as 2019 progresses.

Delta has previously stated the bulk of its capacity growth in 2019 would be geared toward international expansion, but given some of the weakness in the trans-Atlantic, the airline has concluded it could adjust capacity in those markets after the peak summer travel season in the US.

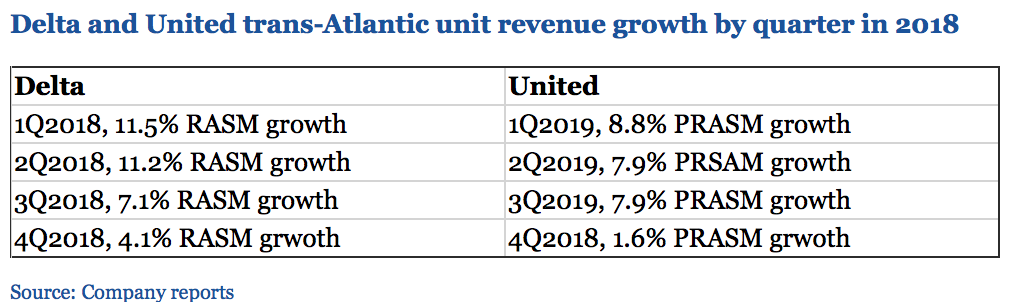

Trans-Atlantic routes were the strongest performers for the large US global network airlines in 2018, helping to offset some weakness in Latin America stemming from currency pressures in Brazil and Argentina. Those airlines also made some gains in trans-Pacific revenue, but the performance was not as strong as trans-Atlantic markets. During 1Q2018 and 2Q2018, Delta posted 11% gains year-on-year in its trans-Atlantic unit revenues.

But by 4Q2018, Delta's revenue growth had fallen to a still respective 4% increase year-on-year, and the airline has stated it sees "cautionary signs" for 1Q2019, noting it expects the trans-Atlantic entity to be the "most challenged".

Domestic unrest in France has affected leisure and corporate performance in the country, Delta executives explained, and that disruption added to currency headwinds, uncertainty over Brexit and the timing of Easter. Together these have resulted in the airline forecasting a modest negative trans-Atlantic unit revenue performance in 1Q2019.

Based on early bookings, Delta believes it should post a strong performance in the trans-Atlantic for the US summer high season, but also cautioned it was watching the region closely, and would adjust its capacity during the shoulder periods if necessary.

United's trans-Atlantic passenger unit revenues fell from 8.8% growth year-on-year in 1Q2018 to a 1.6% increase during 4Q2018. The company's management concluded after two years of strong trans-Atlantic PRASM growth in the market, unit revenue increases moderated during the last three months of 2018.

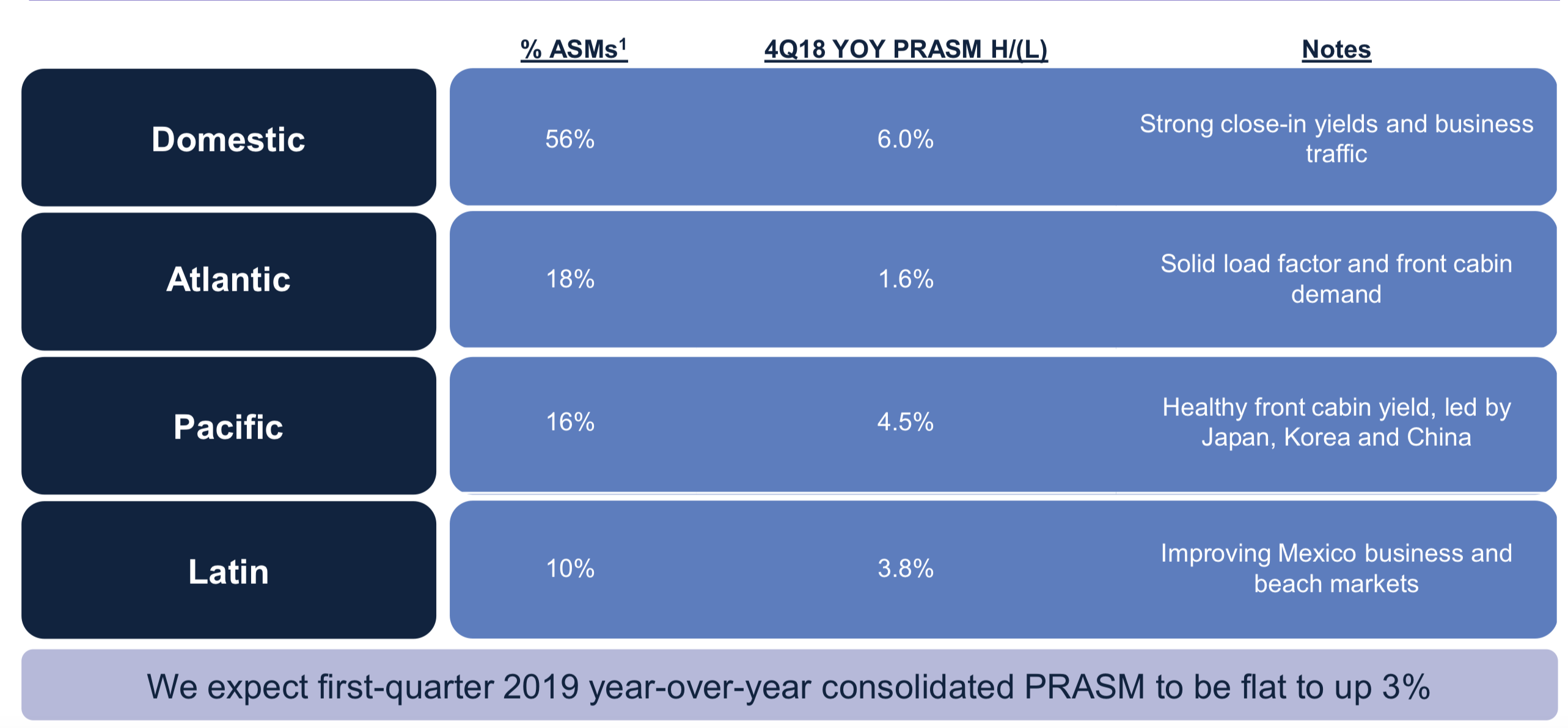

The airline calculated its load factors in the trans-Atlantic increased by 5.2ppt year-on-year in 4Q2018, but the growth in loads was not strong enough compensate for declining close-in yields.

United's departing international ASKs as of mid-Jan-2019 are slightly less concentrated than Delta's, with roughly 29% deployed to Western Europe and 28% to Northeast Asia. It forecasts continuing weakness in coach class on trans-Atlantic routes, which will result in slower PRASM growth in the market over the coming months.

After a banner year in the trans-Atlantic market, it seems as if US airlines are steeling themselves for more tempered results.