Summary:

- Air China will launch a three times weekly link between Chengdu and London Gatwick from 03-Jul-2018 using an Airbus A330-300;

- The new service represents the return of non-stop flights between the Chinese city and London after British Airways suspended its own flights from London Heathrow in Jan-2017 after just over three years of operation;

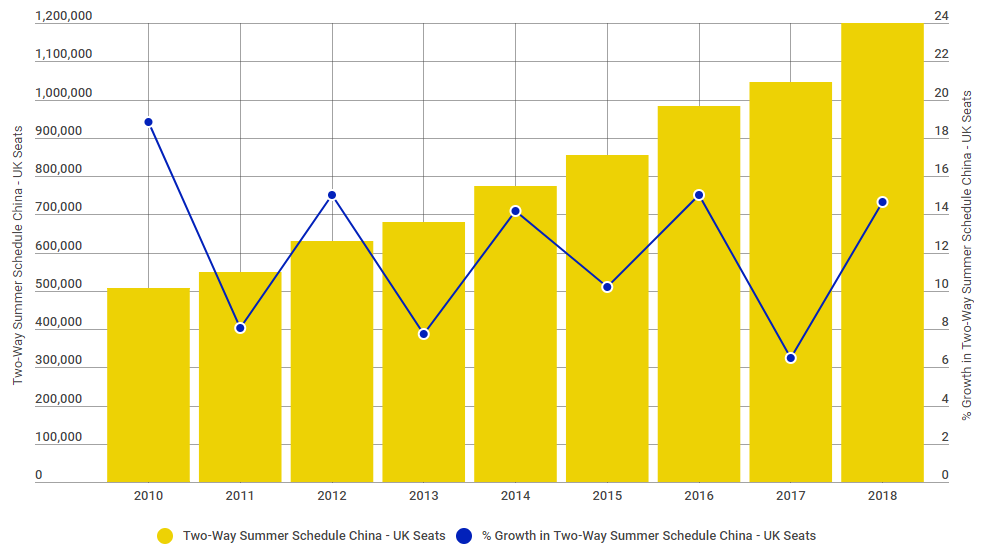

- The number of scheduled departures between China and the UK will be up 10.7% this summer versus the same schedule period last year, with non-stop capacity up 14.6%;

- From this year, ten mainland China markets are now directly linked to London with non-stop flights - Beijing, Changsha, Chengdu, Chongqing, Guangzhou, Qingdao, Sanya, Shanghai, Wuhan and Xian.

There has been a plethora of new arrivals into the China - Europe market over the past couple of years. Alongside the heavyweights of Air China, China Eastern Airlines and China Southern Airlines serving their respective Beijing, Shanghai and Guangzhou hubs, the likes of Hainan Airlines and affiliated operators Beijing Capital Airlines and Tianjin Airlines have entered the arena.

In the UK market in particular there has been a notable shift upwards in connectivity with China. For years, Heathrow Airport officials have lamented about the need for additional capacity to allow London to be as well connected to China as other major hubs across Europe. That is starting to now take effect as alongside Beijing, Guangzhou and Shanghai, from this month the mainland cities of Changsha, Qingdao, Wuhan and Xian are connected to the London hub by non-stop flights, while Sanya services will arrive in Jul-2018. Chongqing and Tianjin are also connected to London via Gatwick Airport, while Manchester and Edinburgh (from Jun-2018 in conjunction with Dublin) are also linked to Beijing.

In fact the number of scheduled departures between China and the UK will be up 10.7% this summer versus the same schedule period last year, with non-stop capacity up 14.6%. Interestingly though, only two of the ten Chinese markets with non-stop links to London are served by UK airlines - namely Beijing by British Airways and Shanghai by British Airways and Virgin Atlantic Airways. The UK airlines account for just 33.8% of summer departures and 31.4% of summer capacity and perfectly highlight the dynamics of the market.

CHART - System capacity between China and the UK has taken off this decade with more than a doubling of available two-way non-stop seats since 2010 Source: The Blue Swan Daily and OAG

Source: The Blue Swan Daily and OAG

Flows between China and most European markets are heavily weighted to the outbound Chinese market and with their own European networks blunted by the low demand and limited feed on the Chinese side of the route, it can be more of a commercial challenge for European airlines to sustainably serve China's emerging secondary cities. A number of global markets are heavily impacted by one-way passenger flows, but as British Airways will testify with its previous service between London Heathrow and Chengdu, the weighting on this route was so heavy it made it not commercially viable to operate.

British Airways had launched the route to a big fanfare (and a Panda painted aircraft) in Sep-2013 but it consistently struggled to fill the aircraft, firstly cutting back aircraft size and frequency and then closing the route in Jan-2017. After a year-and-a-half hiatus Air China will return flights between the cities from 03-Jul-2018 with a three times weekly operation using an Airbus A330-300 in a 285 passenger layout, including 30 Business Class and 255 Economy seats

With its new Chengdu - London service Air China believes it will be able to better serve the passenger demand with a significant feed into Chengdu's Shuangliu International Airport. The new flight will also serve Gatwick Airport in the UK capital as Air China has no interest in onward connections out of London. This will provide operational cost benefits versus flying into Heathrow and allow it to operate a preferred flight schedule, rather than being limited by available slots.

A new study from Frontier Economics 'The Economic Impact of Connections to China' has highlighted the value of non-stop air connectivity to China. Much has been highlighted over recent years about the potential of the huge outbound market from China and their significant spend, but this study now puts a price on this market. In the case of London Heathrow direct flights between London Heathrow and China contribute GBP510 million per year in GDP to the UK economy and create 14,550 jobs. The Hong Kong links alone are responsible for GBP315m of this contribution, followed by Beijing and Shanghai.

https://corporatetravelcommunity.com/london-heathrow-routes-to-china-worth-gbp510-million-to-uk-economy/

A recent study from Frontier Economics 'The Economic Impact of Connections to China' highlighted the value of non-stop air connectivity between China and the UK. Much has been highlighted over recent years about the potential of the huge outbound market from China and their significant spend, but this study finally put a price on this market. In the case of London Heathrow direct flights between London Heathrow and China (including Hong Kong) contribute GBP510 million per year in GDP to the UK economy and create 14,550 jobs.

China was the UK's 6th largest trading partner for exports last year behind only the USA, Germany, France, the Netherlands, and Ireland. Exports to China over this period were worth an estimated GBP15.3 billion. UK imports from China during the same period were worth GBP38.4 billion. The value of UK imports from China was second largest, behind only Germany. Chinese investment in the UK reached USD20.8 billion in 2017, up from USD9.2 billion in 2016.